Global LCD Glass Market Size, Growth & Revenue 2025-2034

Global LCD Glass Market is segmented by Product Type (Alkali-Free Glass, Low-Alkali Glass, High-Alkali Glass, Ultra-Thin Glass, Specialty Glass), Application (Televisions, Smartphones & Tablets, Automotive Displays, Monitors & Laptops, Industrial & Public Displays), Display Type (TFT (Thin-Film Transistor), IPS (In-Plane Switching), VA (Vertical Alignment), TN (Twisted Nematic), STN (Super-Twisted Nematic)), Thickness (<0.3 mm, 0.3-0.5 mm, 0.5-0.7 mm, >0.7 mm), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Executive Summary

The global LCD Glass market is defined by its critical role as the foundational substrate for Liquid Crystal Displays, encompassing various glass types essential for optical clarity, thermal stability, and mechanical strength in diverse electronic devices.

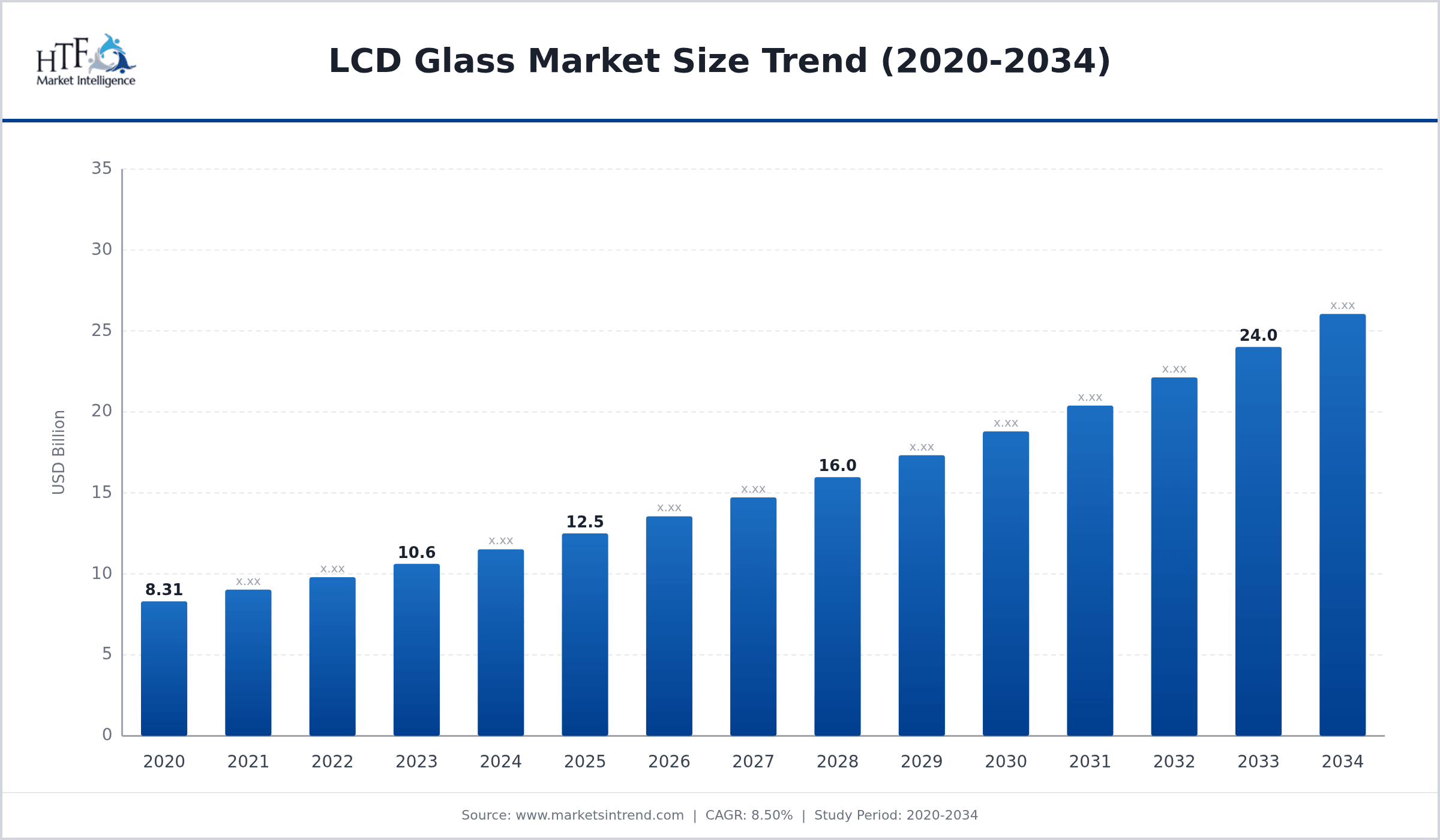

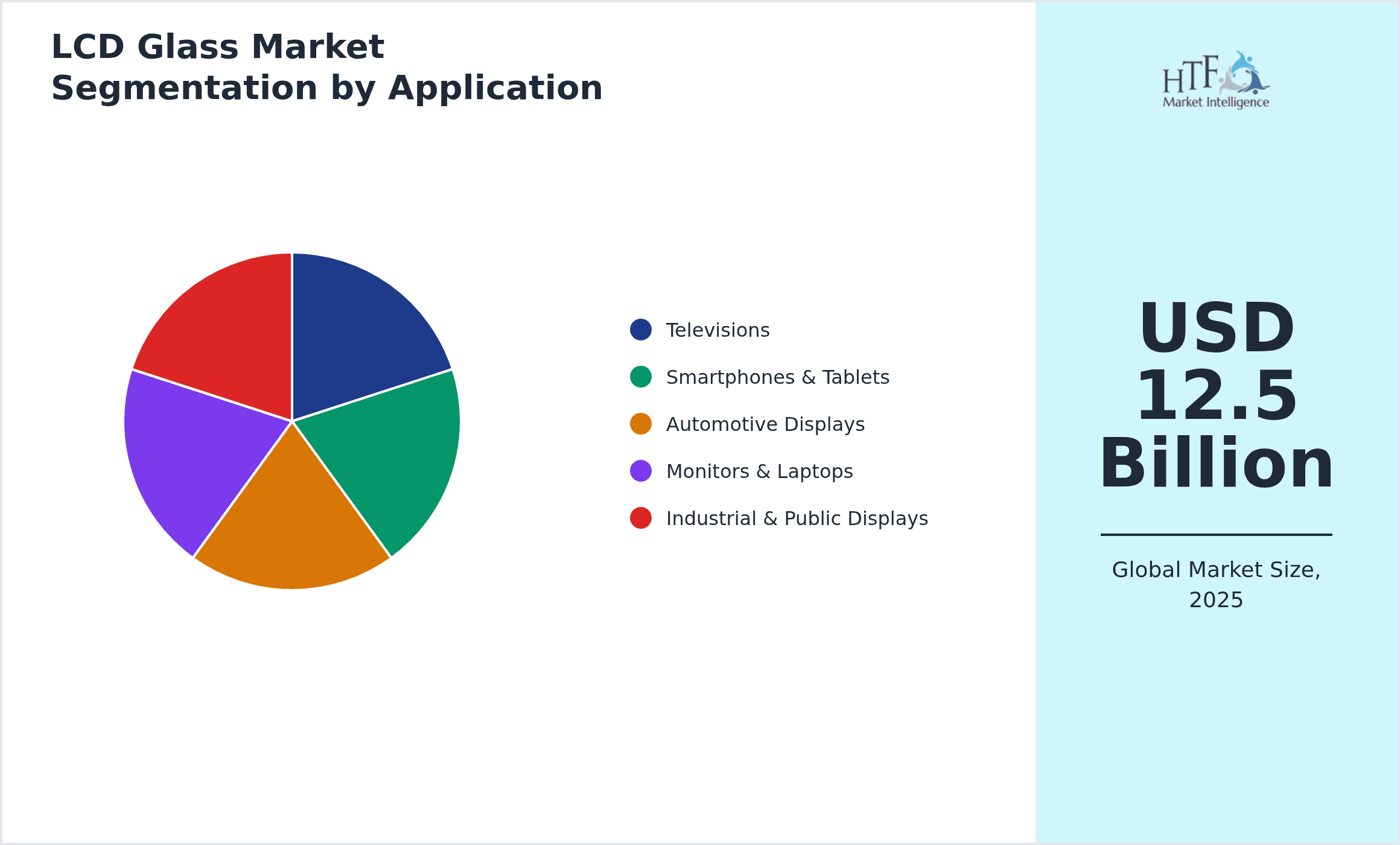

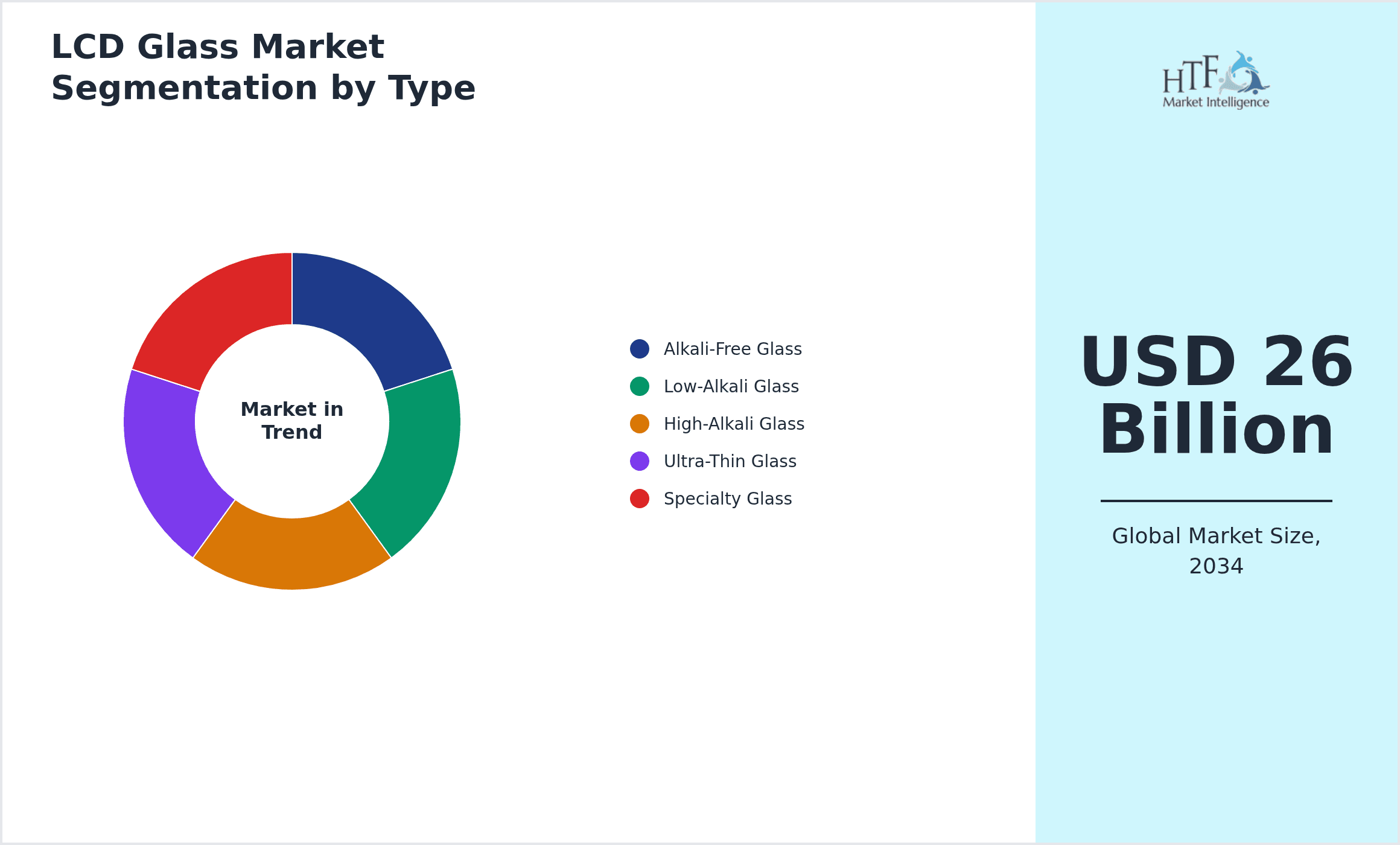

The market is projected to reach USD 26.0 Billion by 2034, growing at a robust CAGR of 8.5% from USD 12.5 Billion in 2025, driven by surging demand for high-resolution displays in consumer electronics and automotive sectors.

LCD glass provides significant value by enabling the production of high-performance, cost-effective displays crucial for a wide range of industries, including consumer electronics, automotive, and industrial automation.

Competitive Landscape

The global LCD glass market is characterized by intense competition among a few dominant players who leverage advanced manufacturing techniques, extensive R&D investments, and strategic partnerships to maintain market leadership. Key competitive strategies include continuous innovation in glass composition for improved performance, enhanced durability, and reduced thickness, alongside optimizing production processes to achieve economies of scale and cost efficiency. Market positioning is heavily influenced by technological prowess in producing high-quality substrates for advanced display technologies, with companies often engaging in long-term supply agreements with major display panel manufacturers. Strategic collaborations and occasional mergers and acquisitions are observed, aiming to expand geographic reach, diversify product portfolios, and consolidate market share. Differentiation often comes from specialized glass properties tailored for specific applications, such as ultra-thin glass for mobile devices or robust glass for automotive displays, while pricing strategies are balanced between premium offerings for high-performance products and competitive rates for mass-market segments. Entry barriers are significant due to the high capital expenditure required for advanced manufacturing facilities and the necessity for deep technical expertise, leading to a concentrated market where a handful of global leaders dictate trends and innovation.

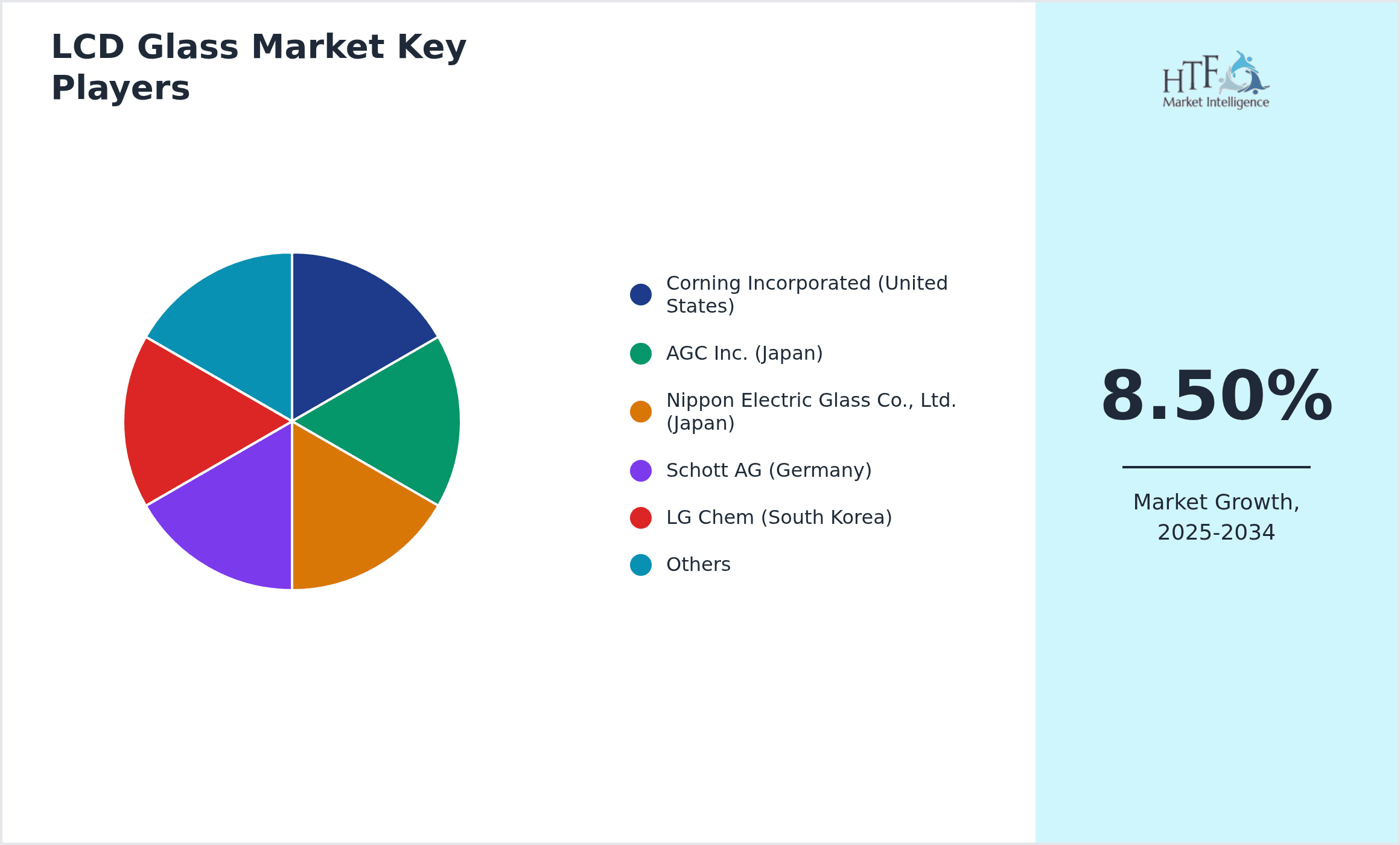

LCD Glass Market Key Players

- •Corning Incorporated (United States)

- •AGC Inc. (Japan)

- •Nippon Electric Glass Co., Ltd. (Japan)

- •Schott AG (Germany)

- •LG Chem (South Korea)

- •Samsung Display (South Korea)

- •BOE Technology Group Co., Ltd. (China)

- •China Star Optoelectronics Technology (CSOT) (China)

- •Innolux Corporation (Taiwan)

- •AU Optronics Corp. (AUO) (Taiwan)

- •Visionox Technology Inc. (China)

- •Tianma Microelectronics Co., Ltd. (China)

- •HKC Display (China)

- •E Ink Holdings Inc. (Taiwan)

- •JOLED Inc. (Japan)

- •Merck KGaA (Germany)

- •Sumitomo Chemical Co., Ltd. (Japan)

- •Dai Nippon Printing Co., Ltd. (Japan)

- •Toppan Printing Co., Ltd. (Japan)

- •Futaba Corporation (Japan)

- •Kyocera Corporation (Japan)

- •Sharp Corporation (Japan)

- •Sony Corporation (Japan)

- •Panasonic Corporation (Japan)

- •Asahi Glass Foundation (Japan)

Market Breakdown

- •By Product Type

- •Alkali-Free Glass

- •Low-Alkali Glass

- •High-Alkali Glass

- •Ultra-Thin Glass

- •Specialty Glass

- •By Application

- •Televisions

- •Smartphones & Tablets

- •Automotive Displays

- •Monitors & Laptops

- •Industrial & Public Displays

- •By Display Type

- •TFT (Thin-Film Transistor)

- •IPS (In-Plane Switching)

- •VA (Vertical Alignment)

- •TN (Twisted Nematic)

- •STN (Super-Twisted Nematic)

- •By Thickness

- •<0.3 mm

- •0.3-0.5 mm

- •0.5-0.7 mm

- •>0.7 mm

Growth Dynamics

The increasing global demand for high-resolution and larger-sized displays in consumer electronics like televisions and smartphones significantly drives the LCD glass market.

Rapid advancements in automotive display technology, including larger infotainment screens and digital dashboards, boost the adoption of specialized LCD glass.

The expansion of industrial and public display applications, such as digital signage and medical equipment, contributes to sustained market growth for durable LCD glass.

Technological innovations leading to thinner, lighter, and more robust LCD glass substrates enhance product appeal and expand application possibilities.

The growing trend of smart homes and connected devices fuels the demand for integrated displays, indirectly supporting the LCD glass market.

Government initiatives in emerging economies promoting digital infrastructure and local manufacturing capabilities further stimulate the demand for display components.

The competitive pricing of LCD technology compared to alternatives ensures its continued preference in various cost-sensitive market segments.

Market Trends

- •There is a notable trend towards ultra-thin and lightweight LCD glass, driven by the demand for sleeker and more portable electronic devices.

- •The integration of advanced functionalities like touch sensitivity and enhanced durability features is becoming standard in modern LCD glass products.

- •Increasing adoption of eco-friendly manufacturing processes and recyclable glass materials reflects a growing emphasis on sustainability within the industry.

- •The development of specialized glass for higher refresh rates and improved optical performance caters to the gaming and professional display segments.

- •Strategic collaborations between glass manufacturers and display panel makers are fostering innovation and accelerating product development cycles.

- •The shift towards larger format displays in both consumer and commercial applications drives the need for bigger and more uniform LCD glass substrates.

- •Mini-LED and Micro-LED backlighting technologies are influencing the requirements for LCD glass, pushing for higher precision and thermal management capabilities.

Market Opportunities

- •The burgeoning market for foldable and rollable displays presents significant opportunities for the development of flexible LCD glass substrates, expanding beyond traditional rigid designs.

- •Untapped potential exists in emerging markets, particularly in Asia-Pacific and Latin America, where increasing disposable incomes are fueling demand for consumer electronics.

- •Innovations in advanced display technologies, such as improved anti-glare coatings and anti-reflective properties, offer avenues for product differentiation and premium offerings.

- •Expansion into niche applications like smart mirrors, augmented reality devices, and transparent displays provides new growth frontiers for LCD glass manufacturers.

- •Developing cost-effective manufacturing processes for large-generation glass substrates can enhance market competitiveness and address the demand for larger displays.

- •Strategic partnerships with automotive OEMs to co-develop integrated, high-durability LCD glass solutions for next-generation vehicle cockpits represent a lucrative opportunity.

- •Investing in R&D for sustainable and eco-friendly LCD glass production methods can attract environmentally conscious consumers and comply with future regulations.

Market Challenges

- •The intense competition from alternative display technologies, such as OLED and Micro-LED, poses a significant challenge to the long-term dominance of LCD glass in high-end applications.

- •Fluctuations in raw material prices, particularly for silica and other key components, can impact manufacturing costs and profitability for LCD glass producers.

- •The high capital expenditure required for setting up and upgrading LCD glass manufacturing facilities acts as a substantial barrier to entry for new market players.

- •Achieving higher levels of optical purity and defect-free production in larger and thinner glass substrates remains a persistent technical challenge.

- •Supply chain disruptions, including geopolitical tensions and natural disasters, can severely affect the global availability and timely delivery of LCD glass.

- •The rapid pace of technological obsolescence in the display industry necessitates continuous investment in R&D, adding pressure on manufacturers' financial resources.

- •Increasing environmental regulations regarding energy consumption and waste disposal during glass production present compliance challenges and potentially higher operational costs.

Regulatory Framework

- •The European Union's Restriction of Hazardous Substances (RoHS) Directive, updated in 2020, mandates limitations on certain hazardous substances in electronic equipment, including display components, influencing LCD glass material composition.

- •Various national and international standards, such as those from the International Electrotechnical Commission (IEC), govern the safety and performance characteristics of LCD panels and their glass substrates, ensuring product quality and consumer protection.

- •Environmental protection agencies globally enforce regulations concerning industrial emissions and wastewater treatment from glass manufacturing plants, driving investments in cleaner production technologies.

- •In Asia-Pacific, particularly China and South Korea, governments have introduced policies and incentives during 2020-2025 to promote domestic display component manufacturing, including LCD glass, aiming for self-sufficiency and technological leadership.

- •Trade policies and tariffs imposed by countries like the United States and China on imported electronic components can impact the global supply chain and pricing of LCD glass, affecting market dynamics.

Market Intelligence

- •15th March 2025, Corning Incorporated announced a significant investment in expanding its Gen 10.5 LCD glass substrate manufacturing capacity in China, aiming to meet the escalating demand for large-sized television panels. This strategic move, valued at over USD 500 million, will bolster Corning's ability to supply advanced, high-quality glass to key display manufacturers in the region, ensuring a stable and efficient supply chain for the rapidly growing market of 65-inch and larger televisions. The expansion focuses on increasing production efficiency and integrating cutting-edge technologies to produce ultra-flat and defect-free glass, crucial for next-generation displays.

- •22nd January 2025, AGC Inc. unveiled its new line of ultra-thin, high-strength LCD glass designed specifically for automotive interior displays at CES 2025 in Las Vegas. This innovative product, named 'AutoBright Glass,' features enhanced scratch resistance and improved optical clarity under varying light conditions, addressing the stringent durability and visibility requirements of the automotive sector. The glass, available in thicknesses down to 0.3 mm, is engineered to support curved display designs and advanced haptic feedback systems, positioning AGC as a key supplier for the rapidly evolving in-car infotainment and digital cockpit market.

- •10th September 2024, Nippon Electric Glass (NEG) introduced a new alkali-free glass substrate, 'G-Flow 2.0,' optimized for high-performance LTPS (Low-Temperature Polycrystalline Silicon) LCDs and emerging OLED applications. This advanced glass offers superior thermal stability and dimensional accuracy, critical for the precise manufacturing processes of high-resolution and high-refresh-rate displays. NEG's innovation aims to support the development of next-generation smartphones, tablets, and wearable devices that demand exceptional visual quality and energy efficiency, further solidifying its position in the premium display glass segment.

- •5th July 2024, Schott AG announced a strategic partnership with a leading Asian display panel manufacturer to co-develop a new generation of robust LCD glass for industrial and medical applications. This collaboration focuses on creating glass substrates with enhanced chemical resistance and extreme mechanical strength, capable of withstanding harsh operating environments and frequent cleaning protocols. The partnership aims to deliver tailored glass solutions that meet the rigorous durability and reliability standards required for critical industrial control panels and high-precision medical imaging displays, expanding Schott's footprint in specialized display markets.

- •Source: Official company press releases and industry publications.

Regional Outlook

The Asia-Pacific currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Latin America is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 12.5 Billion |

| Forecast Year Market Size | USD 26 Billion |

| CAGR | 8.5% |

| Forecast Period | 2026 to 2034 |

| YoY Growth | 8.5% |

| Fastest Growing Region | Latin America |

| Dominating Region | Asia-Pacific |

| Scope of Report | Market is segmented by Product Type (Alkali-Free Glass, Low-Alkali Glass, High-Alkali Glass, Ultra-Thin Glass, Specialty Glass), Application (Televisions, Smartphones & Tablets, Automotive Displays, Monitors & Laptops, Industrial & Public Displays), Display Type (TFT (Thin-Film Transistor), IPS (In-Plane Switching), VA (Vertical Alignment), TN (Twisted Nematic), STN (Super-Twisted Nematic)), Thickness (<0.3 mm, 0.3-0.5 mm, 0.5-0.7 mm, >0.7 mm) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Corning Incorporated (United States), AGC Inc. (Japan), Nippon Electric Glass Co., Ltd. (Japan), Schott AG (Germany), LG Chem (South Korea), Samsung Display (South Korea), BOE Technology Group Co., Ltd. (China), China Star Optoelectronics Technology (CSOT) (China), Innolux Corporation (Taiwan), AU Optronics Corp. (AUO) (Taiwan), Visionox Technology Inc. (China), Tianma Microelectronics Co., Ltd. (China), HKC Display (China), E Ink Holdings Inc. (Taiwan), JOLED Inc. (Japan), Merck KGaA (Germany), Sumitomo Chemical Co., Ltd. (Japan), Dai Nippon Printing Co., Ltd. (Japan), Toppan Printing Co., Ltd. (Japan), Futaba Corporation (Japan), Kyocera Corporation (Japan), Sharp Corporation (Japan), Sony Corporation (Japan), Panasonic Corporation (Japan), Asahi Glass Foundation (Japan) |

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.